|

Remember

the time you sent $100 to your favorite niece in Germany, or $800 to your sick

mother in India, or the $1,500 to your son for his exchange program in Paris?

The money you sent is part of the mega business of remittances, which in 2008

totaled $328 billion worldwide. The bulk of these remittances are transferred

by foreign workers to family members for household expenses in their home

countries. Remittances are the second largest financial inflow to many developing

nations after trade and are bigger than even international aid or total foreign

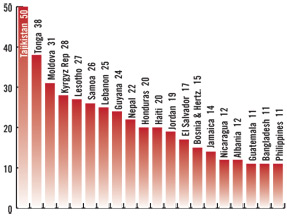

direct investment in India. For countries like Tajikstan, Tonga and Moldova,

remittances constitute between a third to a half of their gross domestic

product. They help fuel social and economic growth in many countries. Most

often expatriates use money transfer organizations (MTOs), such as Western

Union or MoneyGram, to send much-needed money to struggling family members back

home.

|

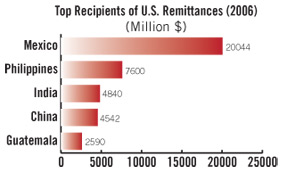

The 25

million non resident Indians are among the largest migrant communities in the

world. Not surprisingly, India is the world’s largest recipient of remittances,

accounting for almost one in six dollars remitted worldwide. The $52 billion

remitted by overseas Indians to India in 2008 constituted nearly 4.2 percent of

India’s gross domestic product. Despite the recession, which analysts’ project

could see remittances decline by 6.1 percent in 2009, the World Bank estimates

that India received close to $49 billion in remittances last year.

One of the

reasons behind the massive surge of remittances to India is the burgeoning

Indian workforce in the Gulf countries. In addition, technical and professional

Indians in Europe, North America and Southeast Asia have become investment

savvy and are investing in Indian real estate and the stock market to take

advantage of the drop in prices and interest rates. Following the crackdown on

informal money transfer services after 9/11, Indians are forced to turn to

formal money transfer services and banks, instead of the informal exchanges of

friends and unlicensed cash agents, whose transactions are not recorded in

World Bank data. As a result of growing competition in this sector, transaction

costs for formal money transfers have dropped markedly in recent years. The

depreciation of the Indian Rupee by almost 25 percent against the U.S. dollar

during the last three quarters of 2008 also led to a surge in remittances.

|

The burdensome

process of wire transfers and international money orders has been replaced by a

plethora of choices in recent years. Today one can use the internet and

electronic fund transfers (EFTs) to send money to anyone anywhere from home

using a bank account, credit or debit card or PayPal. Firewalls, background

checks on employees and encryption of personal information make these

transactions safe. Money transfer options include MTOs, such as Western Union

and MoneyGram, and banks, such as ICICI, CitiBank, State

Bank of India, Wells Fargo andHDFC. Xoom and Remit2India offer

internet focused services. Soon one may be able to transfer money using cell

phones.

Sujit

Kumar Varma, CEO, State Bank of India, New York, says, “The bulk of the inward

remittances are sent by individuals for the purpose of savings (as interest

rates are higher in India), family maintenance and the purchase of real

estate.” SBI is one of the largest retail bank players in the Indian market and

handles the largest volume of remittances within the banking sector. SBI only

handles remittances from its own customers or those registered with the bank,

but the average size of remittances handled by banks tend to be substantially

higher than those handled by MTOs, such as Western Union.

SBI’s U.S.

branches handled $450 million in individual remittances in 2008 and

approximately $320 million in 2009 to India. The volume of remittances has

slowed in the last two years, according to Varma, because of the downturn in

the economy. “In the latter part of 2009, the decline in volumes can also be

attributed to the appreciation of the Indian rupee against the U.S. dollar,

which resulted in people postponing their non essential remittances.”

While India is the

largest recipient of remittances, the United States is the leading source of

remittances. An estimated $47 billion in remittances were sent from America in

2008, according to the World Bank. This is more than twice that of any other

nation except Russia ($26 billion).Nearly half of

U.S. remittances ($25 billion) went to Mexico alone. According to Reserve Bank

of India data (see sidebar), nearly 29 percent of remittances to India come

from North America and 31 percent from the Middle East in 2009. This is a

marked reversal from 2007, when the proportion of remittances to India from

North America was greater than that from the Gulf. Thus, the recession marked a

shift in the geographic distribution of remittances.

| |

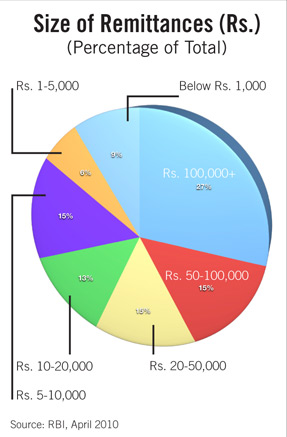

Remittances

to India remained surprisingly resilient during the global recession. A Reserve

Bank of India report in April 2010 reported that “inward remittances in India

have not been impacted significantly by the global economic crisis.” In fact,

notwithstanding the fiscal crisis in Dubai, where the construction sector was

hit hard, with devastating impact on migrant workers, especially from Kerala,

remittances were hardly dented. Many immigrants cut their own expenditures, by

sharing accommodation, for instance, so they could continue to send money home.

Western

Union, the world’s largest money-transfer company, continued to experience

robust growth in the India sector. Arti Kumar Caprihan, Vice President of

Product Management, U.S. Outbound to Europe, Middle East and South Asia, for

Western Union, says the primary reason clients remit money is to support

family, living expenses, gifts for birthdays or weddings, education and to buy

properties.

| |

“India

grew 11 percent in revenues and 22 percent in transactions in 2009. In the

Europe, Middle East, South Asia and Africa region, we saw a decline in revenue,

but a 10 percent growth in transactions in 2009 compared to 2008. However, in

the last quarter of 2009 it saw an increase of 6 percent in revenues and 8

percent in transactions. Business is healthy and has been increasing,” says

Caprihan. The rally is fuelled by remittances to rural areas in Punjab, Uttar

Pradesh, Kerala, Rajasthan, Maharashtra, Andhra Pradesh, Tamil Nadu and

Karnataka, which contribute 60 percent of Western Union’s India business.

Western

Union has aggressively courted South Asian consumers in the U.S. market for

years. “We are part of the Indian community and are experts in multi-cultural

marketing,” says Caprihan. The most active regions in India for Western Union

are Punjab, Gujarat and South India. In the United States, its largest NRI

customer base comes from California, New York and New Jersey.

Transaction

costs and exchange rates influence the costs of money transfer services (see

sidebar), but the ubiquity of agent locations give MTOs like Western Union and

MoneyGram a decided edge. Western Union, once best known for telegrams, is now

the world’s largest money transfer service with over $5 billion in annual

revenues. It has 410,000 agent locations and centers in 200 countries,

including 46,000 in the United States. In India, the company boasts over 50,000

agent locations and partners with 14,000 bank branches of the State Bank of

India, Bank of India and HDFC as well as 8,500 postal service locations.

MoneyGram, which is almost a fifth of Western Union’s size, claims 190,000

locations worldwide, nearly 22,000 of them in India.

MTOs have

the advantage of offering money transfer services all over the world. By

contrast, ICICI Bank presently allows remittances only to recipients in India.

Likewise, the internet money transfer service Xoom allows transfers to only

India in South Asia. But banks have the advantage of being the only ones

allowed to transfer outbound money from India. Remittance costs, which include

a base fee as well as foreign exchange rate margins, are typically lower with

banks than with money transfer services, but banks reserve the services for

their own or registered customers. MTOs are far more covenient to use and

speedier in remitting the money (see sidebar).

The Indian

money transfer market is highly fragmented with independent online companies,

large retail banks and money transfer services like Western Union and

MoneyGram. Reserve Bank of India data indicates that the market share of

remittance volume is 55-60 percent with banks, 35 percent with MTOs and 5-10

percent with online providers.

The MTO

space is dominated by two main players — Western Union and MoneyGram — and a

clutch of regional players who are prominent in certain money transfer

corridors. Nearly 60 percent of India’s population does not have bank accounts,

which gives companies like Western Union and MoneyGram a significant advantage.

Western Union caters to nearly 6.6 million customers in India and 60 percent of

its business in India comes from the rural sector. India and China combined

represented nearly 7 percent of Western Union’s 2009 revenues. Globally,

Western Union had a market share of about 16.9 percent in 2008 compared to 3.9

percent for MoneyGram.

| |

Because

banks handle larger ticket remittances, they have a larger share of the

remittance market by volume, even though MTOs have a larger proportion of

transactions. According to Ecommerce Journal, ICICI’s Money2India has a 20

percent market share of the bank remittance market in India, behind State Bank

of India, which is estimated to control a 24 percent share.

According

to SBI’s Varma: “Agencies like Western Union and MoneyGram handle remittances

on cash-to cash basis i.e. outside the banking channels. Such channels are

popular for sending small value remittances. SBI does not handle remittances on

cash basis and all our remittances are on account of our registered users and

account holders. Hence, we strictly follow ‘Know your customer’ (KYC)

guidelines.”

Although

the remittance sector has proven surprisingly resilient in the face of the

global recession, it continues to be beset by grave risks on multiple fronts.

There is still uncertainty about the economic health of countries around the

globe and the hiring of immigrants has declined in North America, Europe and

the Gulf. In the United States, for instance, thenumber of H1B visa applicants in 2009 fell to

46,700 against a 65,000 quota. By contrast, in 2007 and 2008 the quota was

exhausted within days of opening. A growing protectionist environment in the

United States is likely to result in thefurther tightening of immigration

laws. Many Indians have already returned to India as the Indian economy offers

them stronger prospects than the U.S. In addition, exchange rates, which proved

advantageous for expat Indians at the start of the economic crisis, are turning

as the dollar and the Euro are hammered. Finally, new technology could displace

traditional money transfer companies and disrupt the industry as a whole.

| Top 10 Recepients of Migrant Remittances 2009 (Billion Dollars) |

| |

| Top 10 Recepients of Migrant Remittances 2009 (Percentage of GDP) |

| |

|

You must be logged in to post a comment Login